Newsroom | Climate risks and adaptation: how private equity funds are moving to action

Recap of the roundtable organised on 7 May 2026 by the Climate Working Group of the France Invest Sustainability Commission, in partnership with Blunomy.

On 7 May, at the France Invest Climate Working Group restitution breakfast, three investors, Clémence Lacharme (ADEME Investissement), Victor Seau (IK Partners) and Antoine Joint (Siparex), shared their experiences on integrating physical climate risks into their investment processes. Here are the key takeaways from these exchanges.

Adaptation: a topic entering investment processes, though not yet systematised

The first observation shared by all three funds is one of genuine growing awareness, but still gradual implementation. Climate adaptation is no longer perceived as a distant or purely regulatory subject: it is beginning to take root in the operational processes of investment teams, from deal selection through to portfolio monitoring.

That said, two persistent barriers remain: a lack of dedicated internal resources, and what Clémence Lacharme described as a "risk culture" gap, a concept still weakly embedded in French companies, where the prevalence of insurance has long allowed executives to avoid anticipating and managing risks themselves. Training CEOs in crisis management, including through emergency simulations, is therefore among the first actions some funds have begun to implement.

What funds have put in place: three key steps

Step 1 - Train and raise awareness, starting with internal teams

Before engaging portfolio companies, funds are first building their own internal expertise. Raising awareness among investment teams is presented as a prerequisite: it is difficult to hold a credible dialogue with executives without having a solid grounding in physical risks and adaptation levers.

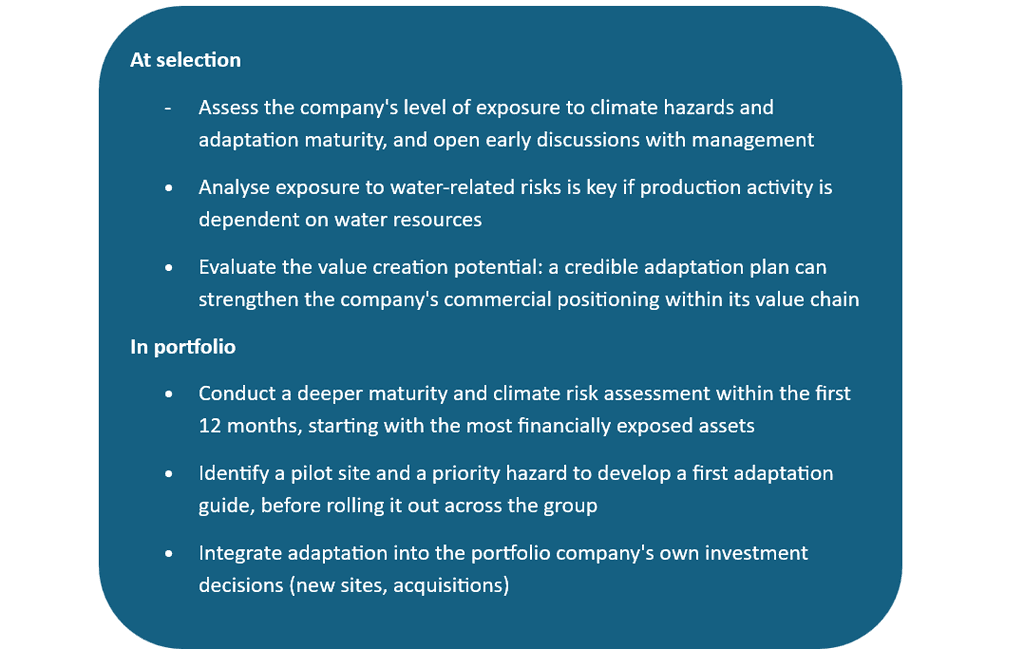

Step 2 - Screen for risks from the pre-investment stage

All three funds have begun integrating physical climate risk analysis into their due diligence processes, using physical risks identification and scoring tools to assess sites' exposure to key hazards: flooding, extreme heat, and fire.

The objective is not to make this a systematic deal-breaker. As participants emphasised, it is generally not a reason to walk away from a deal, but it does allow for early dialogue with executives on concrete, material risks (a site located in a flood zone, a significant dependence on water resources), and for these elements to be integrated into investment committee memos.

A complementary angle is also emerging at this stage: assessing adaptation as a value creation factor. A company that is mature on the topic and equipped with a credible adaptation plan can represent a competitive advantage within its value chain, as some industrial players actively seek out suppliers able to guarantee business continuity in the event of a climate hazard.

Step 3 - Build an adaptation plan with portfolio companies

Once a company is in the portfolio, the challenge is to move from analysis to action. Given the volume of sites to assess, funds have adopted a financial materiality logic: prioritising the most exposed assets by cross-referencing the intensity of climate risks with their weight in the company's revenue.

The IK Partners case study illustrates this approach well. Across a group of 200 private clinics, the fund cross-referenced exposure to extreme climate hazards with the financial importance of each site to identify 5 to 6 critical locations. Adaptation guides were then developed for these pilot sites, organised by hazard type (flooding, fire) and tailored to each site's local context, before being progressively rolled out across the group.

The approach relies on several successive layers of analysis:

· A maturity assessment of the company on the topic (based on a five-level framework)

· An exposure analysis covering physical risks, site by site

· A financial quantification of potential impacts on production processes and business activity

· An adaptation plan co-constructed with operational teams on the ground

This depth of operational engagement is presented as a condition for effectiveness: adaptation solutions must be concrete, grounded in the realities of each site, and owned by the teams responsible for them day to day.

Key priority signals to retain

Several triggers and priorities emerged throughout the discussion:

Water risks deserve particular attention. Dependence on water resources can generate a direct, short-term operational risk for certain industrial activities, making it one of the most concrete and actionable entry points for an adaptation approach.

Adaptation and decarbonation can be aligned. Some adaptation actions are also decarbonation actions, which means that where the two overlap, it becomes possible to reprioritise within a transition plan and maximise the impact of investments made.

A company's climate history is a signal. A company that has already sustained damage from climate hazards is generally more receptive and further along in its awareness. In the absence of such experience, engaging a prospective approach remains more difficult to initiate.

Insurance pressure will change the game. Funds anticipate that insurance will become one of the main accelerators of adaptation in the coming years. France Assureurs estimates that climate-related natural catastrophe losses could reach €143bn in France between 2020 and 2050, nearly doubling compared with the previous 30 years, increasing pressure on insurance affordability and coverage conditions. In this context, demonstrating an asset’s resilience is likely to become a prerequisite for maintaining coverage, accessing financing, and renegotiating premiums.

Adaptation as an investment thesis

Beyond risk management, the discussion also brought to light an offensive reading of the topic. Funds are beginning to identify adaptation as an investment thesis in its own right: solution providers, ecological engineering, network maintenance, water management, infrastructure resilience, operate in fast-growing markets, with global financing needs estimated at between $750 billion and $1.3 trillion per year by 2035*.

For a fund, the question is therefore no longer simply "how do I protect my portfolio from climate risks?”, but also "where are the companies that stand to benefit from the growth of these markets?

Summary: key actions by stage of the investment lifecycle

This article is based on the exchanges from the roundtable of 7 May 2025, organised as part of the restitution of the Climate Working Group of the France Invest Sustainability Commission, in partnership with Blunomy. The deliverables produced through this work, a reference guide on climate adaptation and the Climate Adaptation Toolkit for Private Equity Funds, are available for download at [link].

*Estimated by Blunomy from various sources

Supporting investment funds at every stage of the investment lifecycle

Blunomy works with investment funds to translate climate adaptation from a strategic intention into operational reality, from LP fundraising through to asset management and exit.

Any questions? Get in touch here